PV column

energy

2026/05/08

2026 ESIE Insight: AI enablement and application-driven demand propel energy storage into a new phase of digital-AI convergence (InfoLink Consulting)

In countries around the world, there is a growing trend towards combining renewable energy, energy storage systems, and AI-powered energy management systems.

In this column, we will introduce an article titled “2026 ESIE Insight: AI enablement and application-driven demand propel energy storage into a new phase of digital-AI convergence,” published on April 07, 2026 by InfoLink Consulting, a Taiwanese research and consulting company specializing in renewable energy and technology.

**********

The 14th Energy Storage International Conference and Expo (ESIE 2026) was held at the Capital International Exhibition and Convention Center (CIECC) in Beijing from April 1 to 3, 2026. As one of the largest renewable energy exhibitions in China, the event attracted more than 800 companies across the global energy storage value chain.

While on-site attendance appeared slightly lower than in 2025, engagement at exhibition booths remained highly active, with a notable increase in international participation. Under the influence of Chinese policies such as Document No. 136 and Document No. 114, the energy storage industry is transitioning from a cost-driven model toward value creation.

A key highlight of ESIE 2026 was the integration of AI and energy storage, with product trends pointing toward refined operations and full lifecycle value. Numerous exhibitors showcased related solutions, signaling the beginning of an era of asset-based management for energy storage.

Price trends: Tight cell supply supports price increases; utility-scale ESS prices show recovery

Following the surge in energy storage demand in 4Q25 and slower-than-expected production resumptions at the Jianxiawo mine, lithium carbonate prices rose rapidly. Since 1Q26, lithium carbonate prices have increased sharply followed by high-level fluctuations.

In March, price quotes in China’s LFP energy storage cell market continued to edge up. The sustained strength in lithium carbonate prices throughout 1Q26 has been largely passed through to cell costs.

According to InfoLink’s data, March prices (tax included) were as follows:

- 280 Ah LFP cells: RMB 0.340–0.400/Wh

- 314 Ah LFP cells: RMB 0.335–0.395/Wh

- 100 Ah LFP cells: RMB 0.420–0.475/Wh

If current geopolitical tensions do not materially ease in the short term, elevated cost support for energy storage cells is expected to persist.

Based on China’s domestic ESS tender results in March, the cost pass-through from rising cell prices has become increasingly evident, with both DC-side and AC-side quotes slightly trending upward.

According to InfoLink’s data:

- 2-hour containerized ESS: average bid price of RMB 0.58/Wh

- 4-hour containerized ESS: average bid price of RMB 0.52/Wh

Overall, integrators are facing relatively greater pressure. If upstream material prices decline and ease cell prices, system prices may also trend lower amid intensified competition.

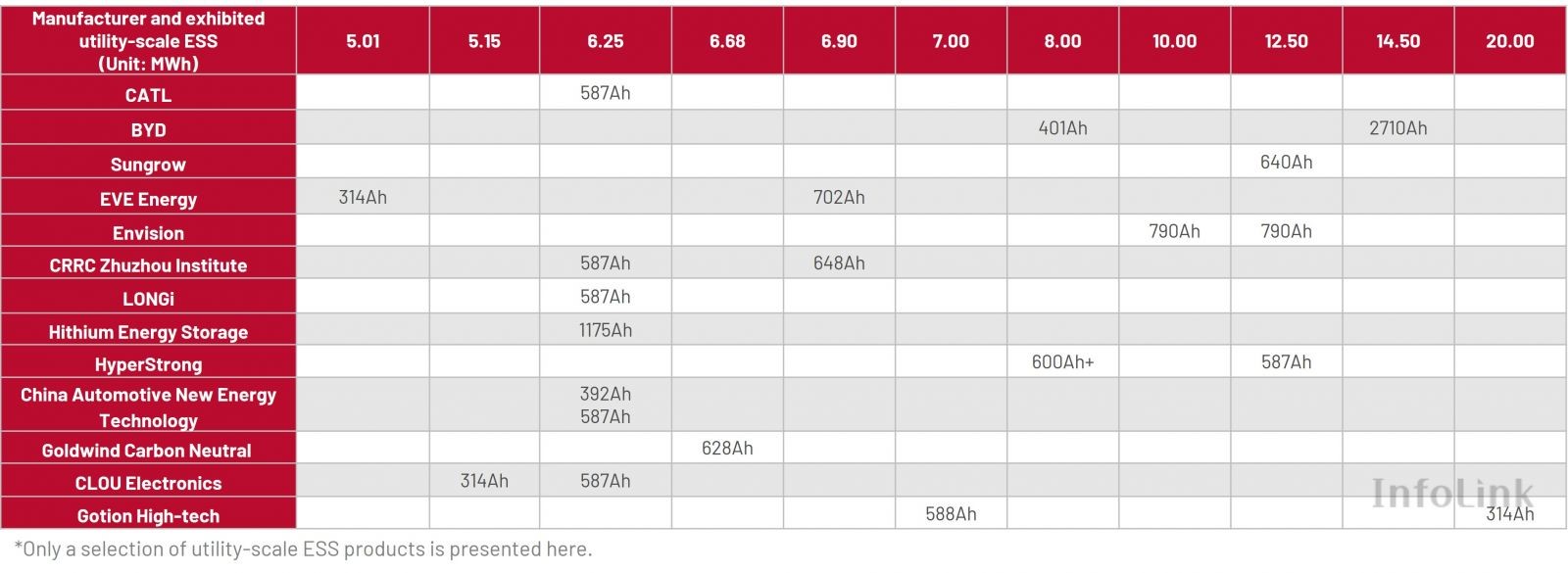

Product trends: 587 Ah and 588 Ah emerge as the dominant next-generation utility-scale energy storage cell formats, with large-capacity designs and “AI + storage” as key themes Utility-scale energy storage cells

At ESIE 2026, 587 Ah and 588 Ah cells were the primary focus among leading cell manufacturers, representing the most concentrated product showcases and attracting the highest level of discussion. In contrast, transitional products such as 392 Ah and previous ~400 Ah formats were still displayed but were no longer the main promotional focus for most companies.

Overall, industry attention has shifted from the previous generation of 300+ Ah and 400+ Ah capacity platforms toward the next-generation mainstream capacity range represented by 587 Ah and 588 Ah cells.

The 587 Ah cell format was first introduced by leading players such as CATL and Hithium, which have already achieved mass production and delivery. At ESIE 2026, 588 Ah emerged as a widely adopted option across multiple manufacturers. Companies including CORNEX, REPT BATTERO, Sunwoda, and CALB prominently showcased 588 Ah products, with most outlining plans for mass production or large-scale delivery within 2026.

Cell format selection above 600 Ah remains relatively fragmented.

Envision unveiled a 790 Ah prismatic wound cell—the largest single-cell capacity to date in the industry—redefining capacity limits from a system-level perspective. This cell format has already entered mass production in early 2026 and is paired with Envision’s latest 12.5 MWh AI-enabled ESS.

Meanwhile, Sungrow is advancing a 684 Ah stacked cell aligned with its next-generation 6.9 MWh ESS architecture. CRRC Zhuzhou Institute introduced a 648 Ah cell paired with a 6.9 MWh ESS solution, while EVE Energy showcased a design that pairs 720 Ah cells with a 6.9 MWh ESS.

Notably, the number of sodium-ion energy storage cells showcased at ESIE 2026 increased significantly compared to previous years. Companies including CATL, EVE Energy, Envision, Great Power, and Shuangdeng all launched new products, indicating that sodium-ion technology is transitioning from technical reserves toward product validation and real-world deployment.

Utility-scale energy storage

Larger cell capacity and higher energy density remain the key product trends at this exhibition. Large-capacity cells showcased by leading manufacturers are directly driving system-level integration upgrades. At the exhibition, BYD showcased its 14.5 MWh Haohan ESS based on 2710 Ah cells; HyperStrong introduced the 8 MWh HyperBlock IV based on 600+ Ah cells; and Envision launched its EN 12.5 MWh AI-powered ESS based on 790 Ah cells, with AI agents expected to enhance lifecycle internal rate of return (IRR) by 4–8%. In addition, LONGi, Hithium, and CRRC Zhuzhou Institute also showcased their latest large-capacity system solutions.

At the exhibition, manufacturers have moved beyond standalone equipment. Competitive differentiation in utility-scale energy storage is shifting from standardized hardware to customer-centric, lifecycle-integrated solutions.

For example, CATL introduced a series of net-zero solutions; Sungrow advanced its “S+ Storage” multi-scenario strategy, shifting its positioning from a standalone equipment supplier to a grid-integrated solutions provider; HyperStrong showcased its “Energy Storage + X” all-scenario solutions; and, notably, Envision launched its AI data center (AIDC) multi-scenario solution, covering grid-side, generation-side, load-side, and control-side applications, with the first 100% renewable-powered data center deployed in Chifeng, Inner Mongolia, in partnership with Tencent.

C&I energy storage: AI-driven intelligent O&M and DT-level ESS emerged as key highlights

The 125 kW / 261 kWh all-in-one system based on 314 Ah cells remains the mainstream product in China’s C&I energy storage market. JD Energy, Shuangdeng, Gotion High-Tech, Jinko Solar, Hoymiles, and Chint Power all highlighted 261 kWh all-in-one systems, with penetration in C&I applications outside China accelerating.

Manufacturers are also scaling toward 400+ kWh C&I all-in-one systems, with Sungrow, JD Energy, Pylontech, and Robestec showcasing such systems based on 314 Ah cells. Hoenergy unveiled a 488 kWh C&I system based on 587 Ah cells, while Ampace presented both a 302 kWh system and a 5 MWh ultra-large-capacity C&I ESS solution.

AI-driven operation and maintenance (O&M) and distribution transformer-level (DT-level) energy storage were key highlights in the C&I segment. Robestec and AlphaESS deployed AI-based software for real-time monitoring, fault prediction, and remote dispatch and control. NR Electric showcased a 261 kWh liquid-cooled C&I all-in-one cabinet for commercial and DT-level applications.

As China’s power market reform deepens, C&I storage is shifting from peak–valley arbitrage to diversified services such as virtual power plants, with future growth driven by both market demand and technical service capabilities.

PCS for energy storage: grid-forming is becoming a standard feature among manufacturers

At this exhibition, grid-forming has become standard across power conversion system (PCS) products. Sungrow, Sineng Electric, Kehua Tech, Soaring Electric, and INPOWER all positioned this technology as a core feature in their latest products. In parallel with the shift toward larger-capacity cells and systems, new PCS products are scaling up in both power rating and integration.

- Sungrow: next-generation 1.725–12.5 MW 1+X modular PCS, designed to actively adapt to complex grid and load conditions.

- Sineng Electric: 1,750 kW grid-forming central PCS.

- CATL: 1.25/1.565 MW centralized PCS, featuring AI-driven air cooling with independent heat exchange; 430 kW liquid-cooled string PCS, which achieves up to 99% conversion efficiency and supports black start and grid-forming control.

- Envision: next-generation AI-adaptive PCS, supporting grid-forming, frequency regulation, and high-reliability AIDC power supply, with certifications from Germany’s VDE FNN, Spain’s REE, and Australia’s AEMO.

- BYD: 2.5–10 MW GC Flux PCS, delivering system-level improvements in power performance and grid support capability.

CATL, Envision, and BYD all launched new PCS products, underscoring that under vertically integrated supply chains, full-stack in-house development and system-level delivery are emerging as core competitive advantages and a shared strategic direction among leading players.

Conclusion

At ESIE 2026, AI integration, grid-forming, and full-scenario customization were the key highlights. On the utility-scale side, 587/588 Ah cells have emerged as the new mainstream format. The debut larger-capacity cells such as 790 Ah and 1,175 Ah formats further reflects the shift toward higher energy density and diversified applications. In the C&I segment, focus was on AI-enabled O&M and DT-level applications, with grid-forming becoming standard in PCS.

Overall, the exhibition underscores two key trends. First, “AI + storage” is evolving from concept to standard practice, covering applications from AI-driven O&M and fault prediction to grid-forming control. Second, manufacturers are accelerating the shift from standalone equipment suppliers to full-stack technology providers and scenario-integrated solution partners. Together, these trends are driving energy storage manufacturers from hardware delivery toward a new phase of AI services and value co-creation.

**********

Chinese energy storage system companies are not only supplying individual components and products, but are also taking a solid approach to product standardization, offering solutions that include energy management systems, and obtaining overseas certifications.

Unfortunately, Japanese companies have almost lost their presence in the global renewable energy market. As specialists in the PV industry, we will contribute to revitalizing the Japanese market and supporting the success of Japanese companies.

Acknowledgments: We would like to thank InfoLink Consulting in Taiwan for introducing us regularly to this useful article.