PV column

Photovoltaic

2026/03/11

Global ranking of solar panel shipments in 2025 (InfoLink Consulting)

In this column, we will introduce the 2025 shipment ranking and analysis of solar panel manufacturers through “InfoLink 2025 global module shipment ranking: Combined shipments reach 536 GW” announced on February 27, 2026 by InfoLink Consulting, a Taiwanese research and consulting company for renewable energy and technology.

**********

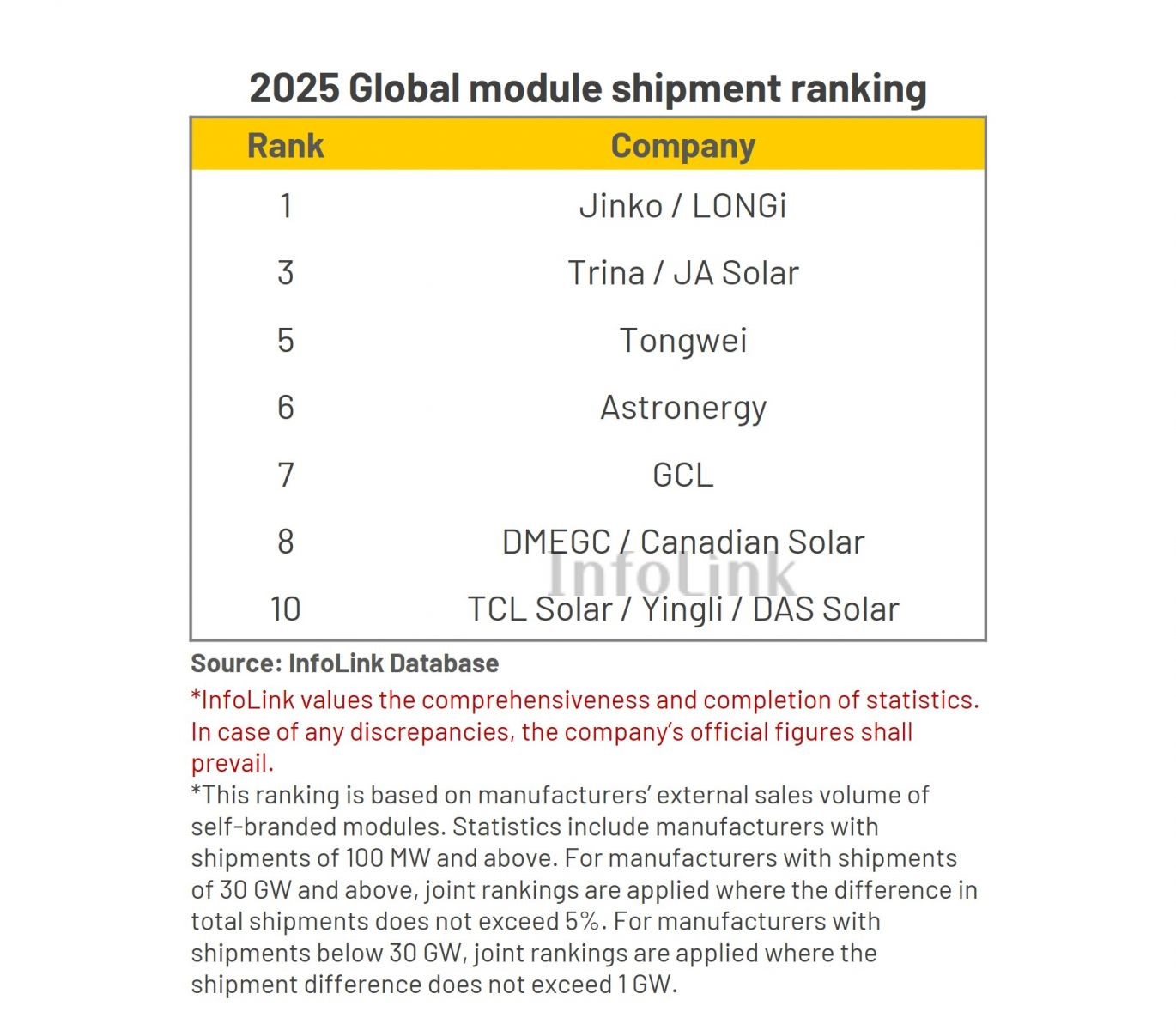

InfoLink 2025 global module shipment ranking: Combined shipments reach 536 GW

Shipment data for this ranking is based on InfoLink’s database and manufacturer surveys and includes companies with shipments of 100 MW and above. Final figures remain subject to the companies’ official disclosures.

In 2025, shipment rankings among lower-tier companies were highly concentrated, with the gap between the highest and lowest shipment volumes among companies below 30 GW narrowing to less than 5 GW.Accordingly, the methodology for handling ties has been revised as follows:

- For companies with shipments of 30 GW and above, the previous rule remains in place, whereby companies are ranked jointly if the difference in total shipments does not exceed 5%.

- For companies with shipments below 30 GW, joint rankings are applied where the shipment difference does not exceed 1 GW.

Tiers 1 and 2: Industry leaders

Based on InfoLink’s market research, total shipments of ranked global module suppliers reached approximately 536 GW in 2025. As shipment volumes were particularly concentrated among lower-tier companies, a total of 12 companies were included in this list.

The leading tier recorded shipment volumes in the range of 80–90 GW. Jinko and LONGi ranked jointly in first place after including shipments from their U.S. module facilities, separated by only a marginal difference.

The second tier recorded shipment volumes in the range of 60–70 GW, with Trina Solar and JA Solar tied in third place.

This ranking has been cross-verified through multiple channels and validated through repeated review. However, given the relatively narrow shipment gaps among leading companies, the top four positions this year formed two tie groups: first and second place were tied, while third and fourth place were also tied.

It should be noted that the shipment figures for the top four companies in this ranking include output from their U.S.-based module manufacturing facilities. Specifically, Jinko’s include output from Jinko Solar (U.S.) Industries, Inc.; LONGi’s shipment figures include output from its subsidiary Illuminate USA; Trina Solar’s include output from T1 Energy Inc.; and JA Solar’s include output from American Panel Solutions (Corning).

The top four companies accounted for approximately 58% of total shipments in this ranking. With 60 GW serving as a clear dividing line, a distinct gap emerged between them and the rest of the ranked suppliers.

The top four companies continue to drive industry development through sustained technological innovation. Jinko has increased investment in its TOPCon 3.0 roadmap, achieving further breakthroughs in module power output. LONGi has expanded the deployment of its BC products, deepening its premium positioning and brand influence. Trina Solar has consolidated its advantage in industry-wide format standardization through its 210/210R series. JA Solar has also steadily advanced the industrialization of TOPCon 3.0 and BC technologies, underscoring its commitment to sustaining competitiveness through continuous technological innovation.

Building on their established scale advantages, these four companies have continued to deepen R&D capabilities and differentiated product positioning, while further strengthening domestic and overseas channel networks to solidify long-term competitive advantages.

Tier 3: Prudent positioning with steady execution

Tier-3 players recorded module shipments at 30–50 GW. The fifth and sixth positions remain unchanged, held by Tongwei and Astronergy, respectively. In contrast to Tier-1 and Tier-2 manufacturers that emphasize technological leadership and forward-looking strategies, Tier-3—serving as the backbone of the industry—generally adopt a more cautious and disciplined operating style in their module businesses. With a follower-oriented and risk-conscious mindset, Tier-3 players focus on strategic positioning under controllable risk conditions.

The strategic orientation of Tier-3 players can be seen from two perspectives.

First, they have adopted a relatively cautious stance toward capacity expansion outside China. While continuing to conduct market research and medium- to long-term strategic scenario planning, they have seldom taken the lead in large-scale capacity expansion outside China amid the accelerating globalization. In 2025, their shipment mix remains primarily supported by the Chinese market.

Second, regarding technology roadmaps and product formats, they generally follow prevailing market trends. This approach enables them to reduce exposure to uncertainties associated with technology iteration and to mitigate the capital expenditure pressures arising from large-scale trial-and-error investments.

From a broader group-level perspective, the PV segment does not constitute the sole core business for either company. Other industrial divisions within their corporate structures continue to provide resources and support. This diversified structure strengthens overall risk resilience and financial stability. At the same time, it leads to a more measured degree of strategic aggressiveness and capital allocation in the PV industry.

Tier 4: Close shipment volumes amid fierce competition

Tier-4 players recorded module shipments at 20–30 GW. GCL ranked seventh. Eighth place was jointly held by DMEGC and Canadian Solar. Tenth place was shared by TCL Solar, Yingli, and DAS Solar.

Within Tier-4, aside from DMEGC (with Europe as its primary overseas market) and Canadian Solar (with a strong presence in North America), most companies remain largely reliant on the Chinese market. Based on cross-verification from multiple sources, shipment volumes among Tier-4 players are extremely close, with the gap between the highest and lowest figures within the tier at less than 5 GW. As a result, rankings in 2026 may still see significant reshuffling.

It is worth noting that TCL Solar’s ranking in this period includes shipments under multiple brands, covering HuanSheng, TCL Solar, TCL PV Tech, SunPower, and Maxeon. If the acquisition and integration of DAS Solar proceed smoothly in 2026, the combined entity—both previously possessing top-ten potential—could advance into a higher tier and further reshape the competitive landscape.

In addition, companies on the margin of this ranking include First Solar, Aiko, and Risen, each with shipments exceeding 10 GW. Notably, these three companies correspond to the primary technology pathways beyond TOPCon—namely thin-film, BC, and HJT technologies; each aims to capitalize on technological differentiation and potentially achieve competitive breakthroughs in the emerging “post-TOPCon” era.

2025 shipments shifted toward non-China markets, while TOPCon maintained its dominant market share.

In 2025, module shipment pacing was volatile. H1 was affected by China’s Document No. 136 policy, while H2 faced uncertainty stemming from anticipated export VAT rebate adjustments. Leading listed module suppliers remained focused in China, with the country accounting for 55% of total shipments and non-China markets 45%. The share of exports from non-China markets increased by three percentage points YoY.

According to China’s customs data, China’s PV module exports reached 267.6 GW in 2025, up approximately 13% YoY. Excluding shipments from manufacturing bases outside of China, the ranked suppliers collectively contributed around 80–85% of total exports, highlighting their scale advantages and channel strength. Leading players have effectively consolidated control over global export market resources.

In non-China markets, beyond traditional demand centers in Asia-Pacific and Europe, many suppliers accelerated expansion into the Middle East and Africa, both of which recorded shipment growth. In contrast, the U.S. market was disrupted by reciprocal tariffs, AD/CVD volatility, FEOC compliance constraints, and OBBBA subsidies phasing down ahead of schedule, posing material challenges to planned capacity expansions for most manufacturers.

From a technology perspective, TOPCon modules became the dominant product among the global top ten suppliers in 2025. TOPCon accounted for almost 95% of shipments among ranked companies, while PERC declined to 1-2%.

As manufacturer Aiko and major HJT suppliers were not included in the ranking, the data do not fully represent the global market share of BC and HJT modules. Rather, they primarily reflect the technology allocation strategies of mainstream suppliers in their shipment portfolios.

From market share to sustained competitiveness: The survival strategy of global leading module suppliers

In 2025, the module industry remained in a downturn. While high shipment volumes demonstrated brand strength and channel reach, long-term sustainability ultimately depended on consistent profitability. The global top ten module suppliers were all vertically integrated manufacturers. While scale provides structural advantages, it also brought higher fixed costs and deeper capital commitments in a loss cycle, resulting in greater operational strain.

At the start of 2026, the year is critical for most PV enterprises. After two consecutive years of negative net profit, a further loss would have triggered ST (special treatment) risk warnings. At this critical juncture, companies are expected to shift their strategic orientation this year.

Although module prices have shown signs of a notable rebound recently, the increase was largely a pass-through effect driven by higher silver prices rather than a fundamental recovery in end-market demand. Against this backdrop, gross margins did not improve in tandem, and overall profitability remained at a subdued level. Demand also remains under pressure. According to InfoLink’s forecast, China’s newly installed capacity in 2026 is projected to decline from 316.57 GW in 2025 to 180-210 GW, a YoY decrease of 34–43%.

Amid expectations of a pronounced demand contraction, the temporary rebound in module prices and the improvement in market sentiment are insufficient to offset structural pressures. Under the new tariff framework, module price levels in many provinces of China are no longer aligned with reasonable return levels for Chinese project investors. In several cases, the internal rate of return (IRR) of PV projects compressed materially, with capital even reallocating to wind power or conventional energy assets.

Overall, the price rebound failed to materially improve industry fundamentals. Profitability on the manufacturing side remains unrecovered, while project returns face mounting pressure. Amid demand contraction and margin compression, 2026 is poised to become a decisive year of accelerated industry differentiation and consolidation.

Previously, competition centered on expanding shipments and securing early-mover advantages. With most regional markets now broadly covered, the industry may need to reconsider how to leverage differentiated products to penetrate niche segments, align more closely with customer needs, and enhance long-term customer stickiness, thereby moving beyond product homogenization and price-led competition.

Reflection on product “price” versus “value” has been intensifying. Companies that balance scale with profit—redirecting competition from price to value and transforming short-term shipment gains into durable competitive moats—will be best positioned to outperform in the next industry upcycle.

**********

The four market leaders (Jinko, LONGi, JA Solar, and Trina Solar) have a combined annual shipment volume of approximately 300 GW, but their hard competition has led to low profit margins, causing them to incur significant losses.

While it will depend on trends in China, the world’s largest solar PV market, we hope that the solar PV market will stabilize in 2026.

Acknowledgments: We would like to thank InfoLink Consulting in Taiwan for introducing us to this useful article.