PV column

energy

2026/04/08

The energy security fallout: from fossil fuel fragility to electric independence (EMBER)

In Japan, attention is likely focused on the Strait of Hormuz as a result of the conflict in the Middle East that began at the end of February 2026. While Japanese news may mention figures such as the proportion of oil in the area, it seems that there is little information that provides a broader perspective on the current global energy situation and the impact of trends in renewable energy. I suspect that most people are unaware that “Japan spends more than 3% of its GDP each year on importing fossil fuels.”

In this column, we will introduce “The energy security fallout: from fossil fuel fragility to electric independence,” published on March 18, 2026, by Ember, a UK energy think tank.

**********

The energy security fallout: from fossil fuel fragility to electric independence

The fragility of global fossil fuel supply underscores why scaling renewables and electrification is essential for lasting energy security.

About the report

This short report presents key data on how the conflict in the Middle East exposes insecurities for economies dependent on imported fossil fuels, and how electrotech – like EVs, solar, wind, batteries and heat pumps – can help to mitigate these risks.

Media highlights

Summary

The fragility of global fossil fuel supply underscores why scaling renewables and electrification is essential for lasting energy security.

- Today’s fossil insecurities: Three-quarters of the world’s population live in fossil-importing countries. Net importers spent $1.7 trillion in 2024. If fuel prices rise, this number rises. For every $10 per barrel increase in oil prices, global net import costs rise by around $160 billion per year.

- Clean energy offers a permanent solution: Scaling electrotech – EVs, renewables and heat pumps – to replace imported fossil fuels in road transport, heating, and power, would enable importers to cut their fossil fuel imports by 70%.

- Electrotech is already at the scale to cushion shocks: The global fleet of electric vehicles avoided oil consumption equivalent to 70% of Iran’s exports in 2025. Global solar growth in 2025 alone could displace gas-fired electricity equivalent to all LNG exports through the Strait of Hormuz that year.

- The lasting consequences: This crisis will accelerate what was already underway. Asia, which imports 40% of its oil through the Strait of Hormuz, now faces the same reckoning Europe did in 2022 — but with increasingly cost-competitive electrotech alternatives available. The bull case for LNG as Asia’s transition fuel is now much weaker. And peak oil has been brought sharply forward: the International Energy Agency has already cut its 2026 demand growth forecast, and the peak it previously put at 2029 may already be here.

“Oil is the Achilles’ heel of the global economy. In particular, Asia’s oil vulnerability has been exposed by the current crisis. This is Asia’s Ukraine moment. Unlike the oil crises of the 1970s, there is now a better alternative. Electric vehicles are increasingly cost-competitive with gasoline cars. Oil volatility means EVs are a common-sense choice for countries wishing to insulate themselves from future shocks.”

1. Today’s fossil insecurities

The closure of the Strait of Hormuz has shut down the world’s most important fossil fuel trade route. The fallout reveals just how deep the world’s fossil dependency runs.

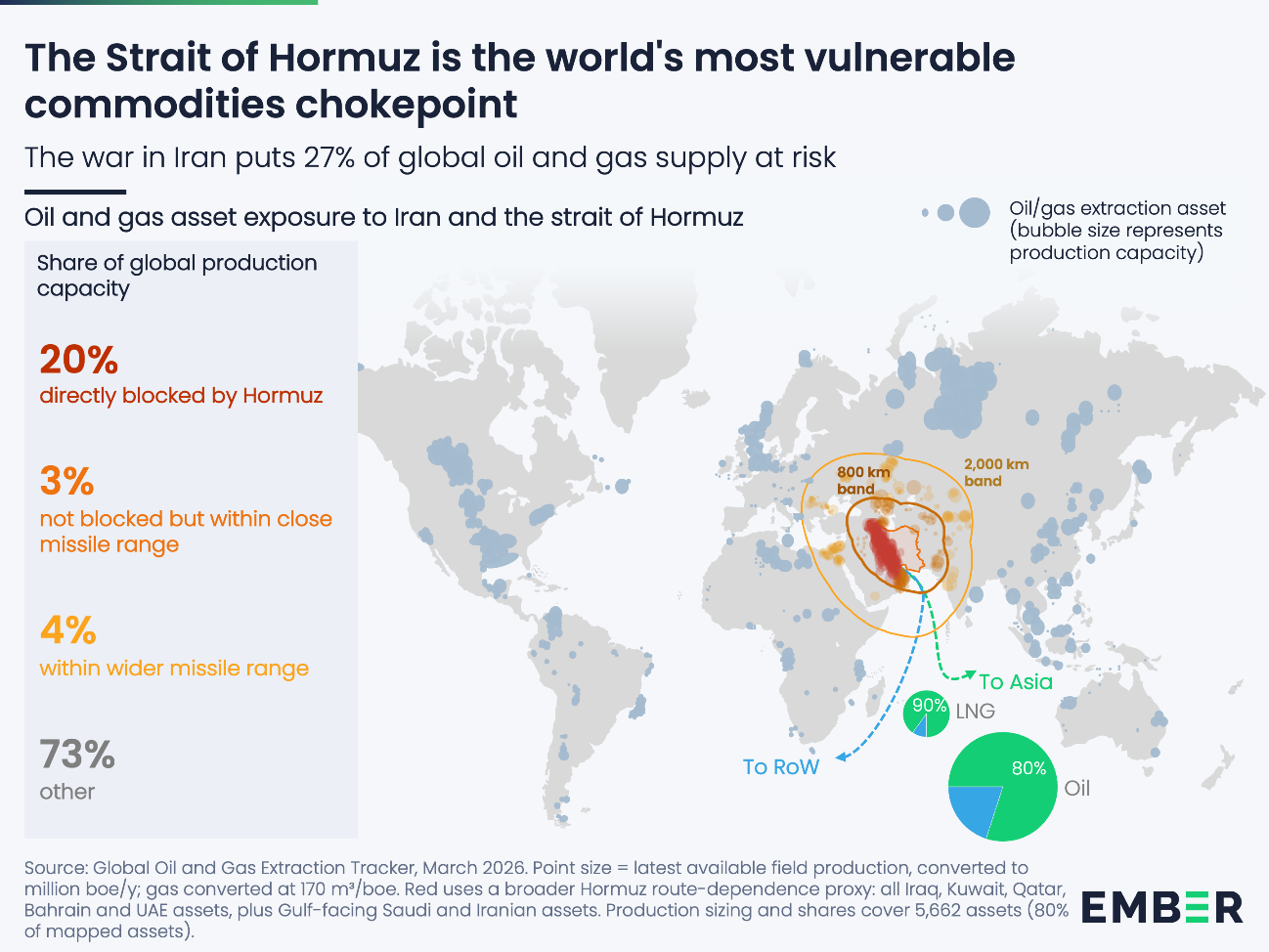

The world’s most vulnerable chokepoint

The Strait of Hormuz is narrow, shallow, and carries a fifth of the world’s oil and LNG. The wider Gulf region, within range of cheap drones, makes up 29% of global oil output and 17% of gas. It is also a major route for trade in fertilisers, aluminium, sulphur, and ammonia. There is no other bottleneck in the global commodity system where so much passes through so little.

Where the 2022 crisis was about Europe and gas, this one is about Asia and oil. 80% of the oil and 90% of the LNG that transits Hormuz is bound for Asian markets. That is roughly 40% of Asian oil demand and over a quarter of Asian LNG imports. Japan, South Korea, India and Thailand all depend on it as their main source of supply.

Yet fossil fuel dependency stretches beyond the countries most dependent on the Strait of Hormuz. The exposure is global, and the import bill is large.

Fossil dependency is widespread and expensive

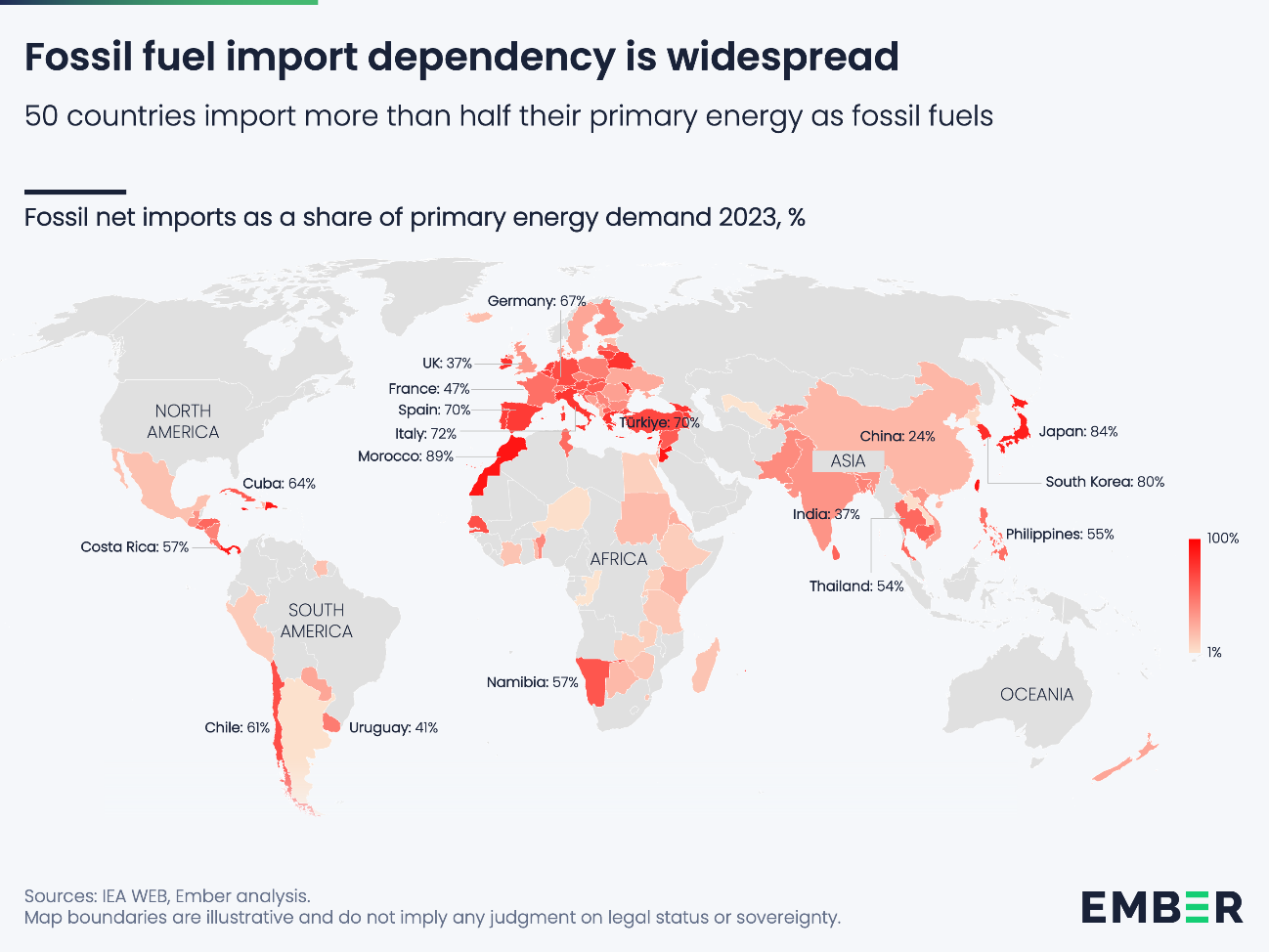

Three-quarters of the world’s population live in net fossil fuel importing countries, according to Ember’s analysis. Fifty countries import over half their primary energy as fossil fuels. Spain, Italy and Germany, for example, import over two-thirds of their energy. Japan and Korea over 80%, India 37% and China a quarter. When trade routes are under threat, these countries are exposed.

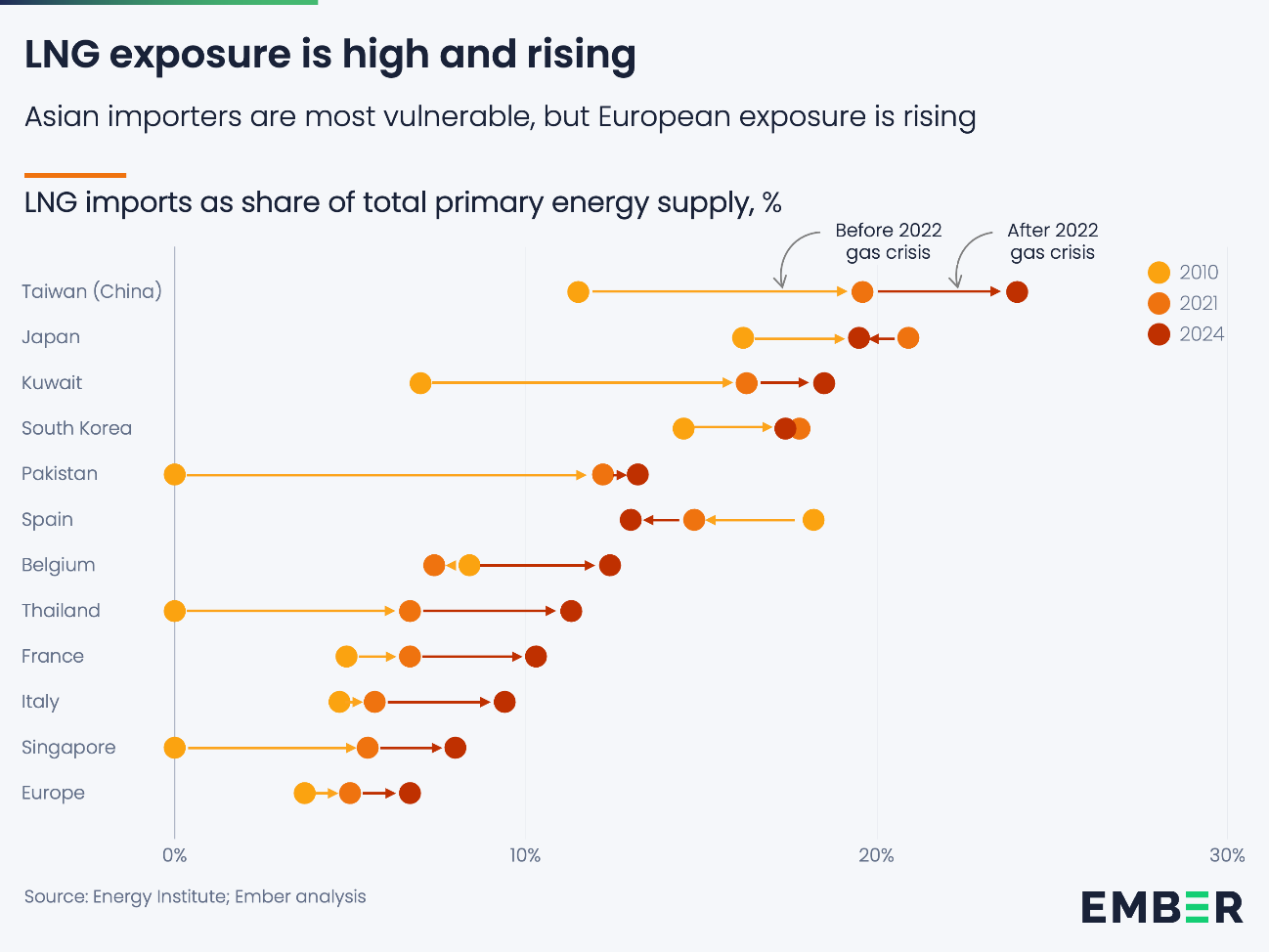

LNG exposure has been rising. About 60% of the world’s population live in LNG net importing countries. In at least nine countries, LNG imports make up over 10% of total energy supply. Taiwan is the most exposed at 24%, followed by Japan at 20% and South Korea at 17%. In several countries, exposure rose after the Ukraine crisis, compounding the impact of Hormuz today.

At the global level, the Gulf’s LNG matters less than its oil. Gulf LNG makes up less than 1% of world primary energy; whereas Gulf oil provides 9%. Analysis of IEA data by Ember shows that 79% of the global population live in oil-importing countries. In 2023, 62 countries imported 99% or more of their oil and 89 countries imported more than 80% of their oil, including Spain (99%), Japan (99%), Germany (96%), Türkiye (92%) and India (87%).

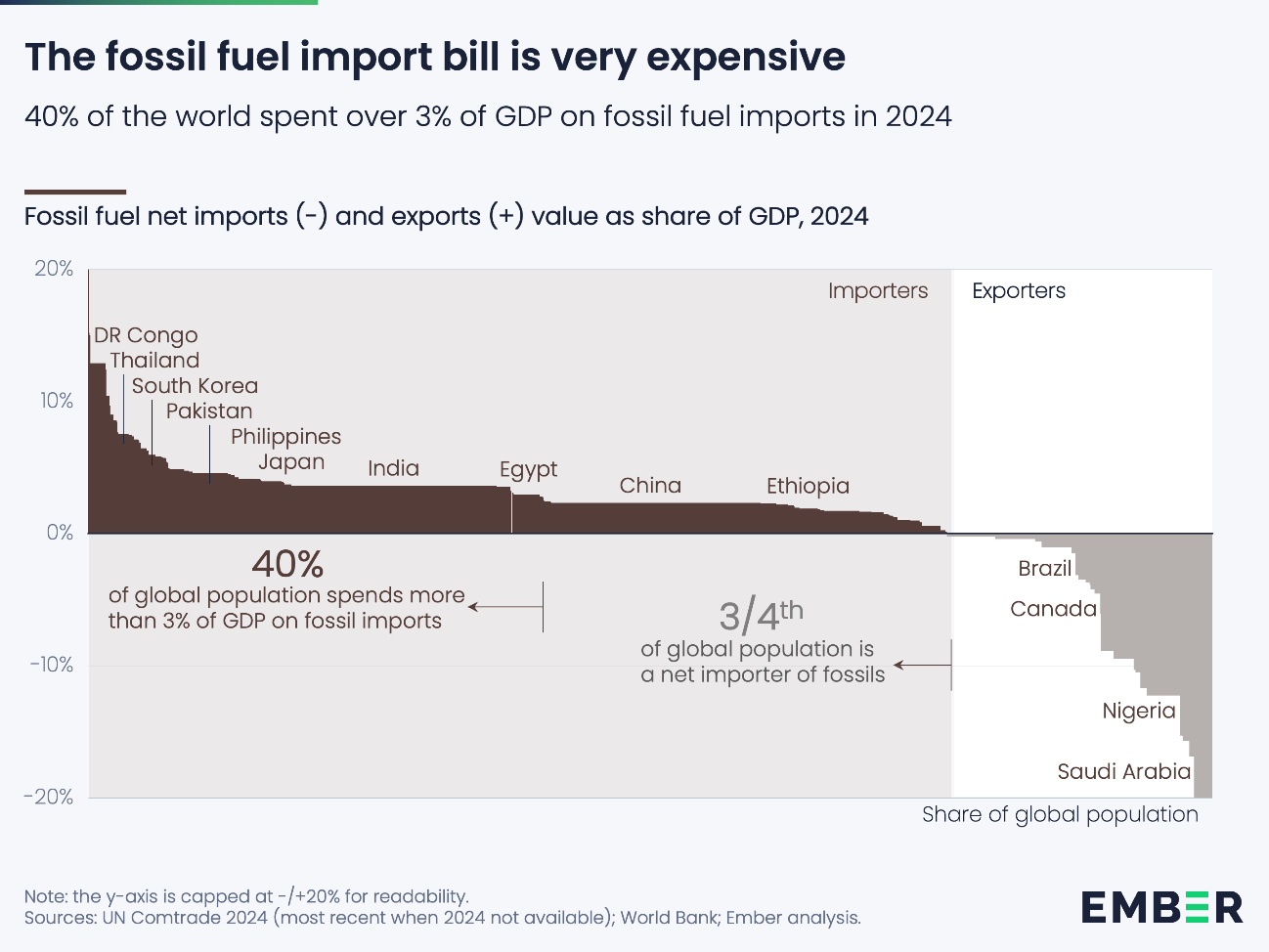

The dependency comes at a high price. Net importers spent $1.7 trillion on fossil fuel imports in 2024. Two-fifths of the global population (92 countries) leak over 3% of GDP abroad in net fossil fuel imports. And as prices rise, so does the bill. For every $10 per barrel increase in the oil price, global net import costs rise by about $160 billion a year. For every $1 per million British thermal unit (MMBtu) increase in the LNG gas price, global net import costs rise by about $20 billion per year.

The impact of rising prices

The first-order impact of a supply disruption is higher prices. These ripple through the wider economy, hit importers and exporters alike, and fall hardest on the poorest.

The price shock is already spreading across the fossil fuel economy. Taking Europe as an example, with jet fuel – much of which is imported directly from the Middle East – prices are up 70% since the war began. Gasoline is up 30%, in line with crude. Wholesale gas is up 61%. Heating oil, which hits rural households fastest, has risen even more. Ethylene, a basic input for plastics and chemicals, is up 20%. Urea, used for fertilisers, is up 27%.

Domestic production offers little by way of shelter. Oil prices are set globally, so a crisis like the closure of the Strait of Hormuz hits producers and importers alike. In Texas, one of the world’s largest oil-exporting regions, gasoline prices rose by over 25% since the war started. That is larger than the price rises seen so far in oil-importing countries like the UK and France. Building up more domestic production does not insulate an economy from a global price shock.

High prices hit the poorest hardest. Low-income households in the US can spend as much as 20% of their disposable income on energy. Poorer economies like Namibia, Thailand, and the DRC spend over 7% of GDP on fossil imports. When supply tightens, the rich bid up prices to get the energy they need – and in doing so price out the poor.

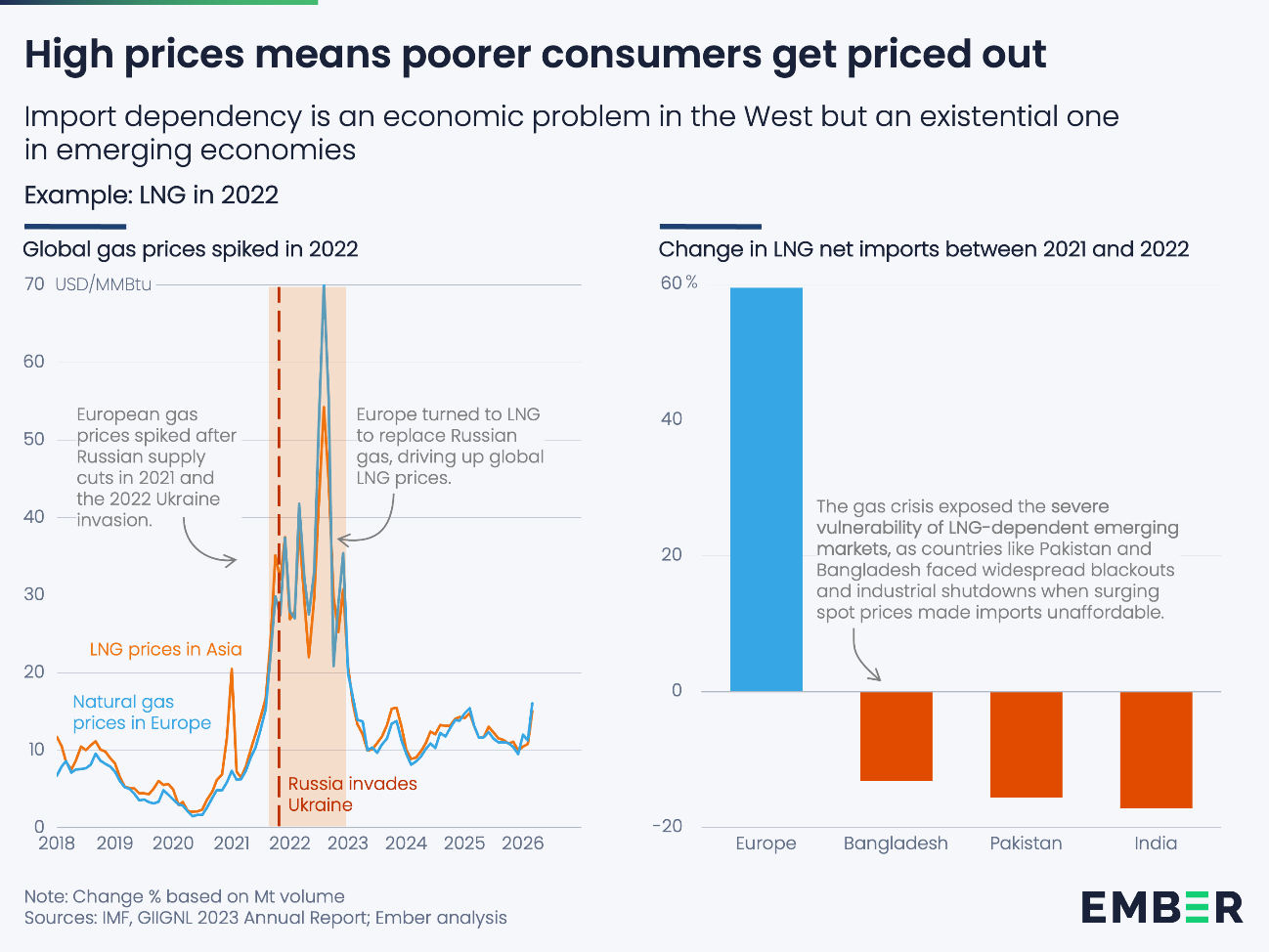

The 2022 crisis showed exactly this. Europe’s LNG net imports rose by nearly 60% as the continent scrambled to replace Russian gas. Bangladesh, Pakistan and India, meanwhile, saw their LNG imports fall by 13–17%. They did not cut back by choice. They were outbid.

Volatility is structural, not episodic

This is the second major fossil fuel crisis in four years. The question is whether this is a run of bad luck, or whether we are in a new world where such crises are structurally more likely.

The underlying shifts point to the latter. Most notably the change in US incentives. In the early 2010s, the United States was the world’s largest petroleum importer. Now it is a net exporter as we noted in Energy security in an insecure world. That changes its incentives. The pax Americana – the US-led security framework that underwrote a global economy built on the constant, just-in-time arrival of fossil fuels – appears to be waning. The architecture that kept fossil fuels flowing reliably for seven decades is starting to show cracks.

This alone would be cause for concern. But it coincides with a broader deterioration. Global armed conflicts are on the rise. Tariff levels and trade uncertainty are now at their highest in decades. Oil volatility indices have risen to levels that, outside 2022, have not been seen this millennium. As the world gets less stable, the risk of such dependency becomes less tolerable. The fossil fuel system, reliant on continuous trade through a handful of chokepoints, is becoming more fragile, not less.

2. The new electrotech alternative

In the past, there were few alternatives to fossil fuel dependency. Now there is electrotech – EVs, solar, wind, batteries, and heat pumps. Countries can affordably slash imported fuels across the whole economy. For many, this is already cushioning the blow.

Every country can be energy independent with electrotech

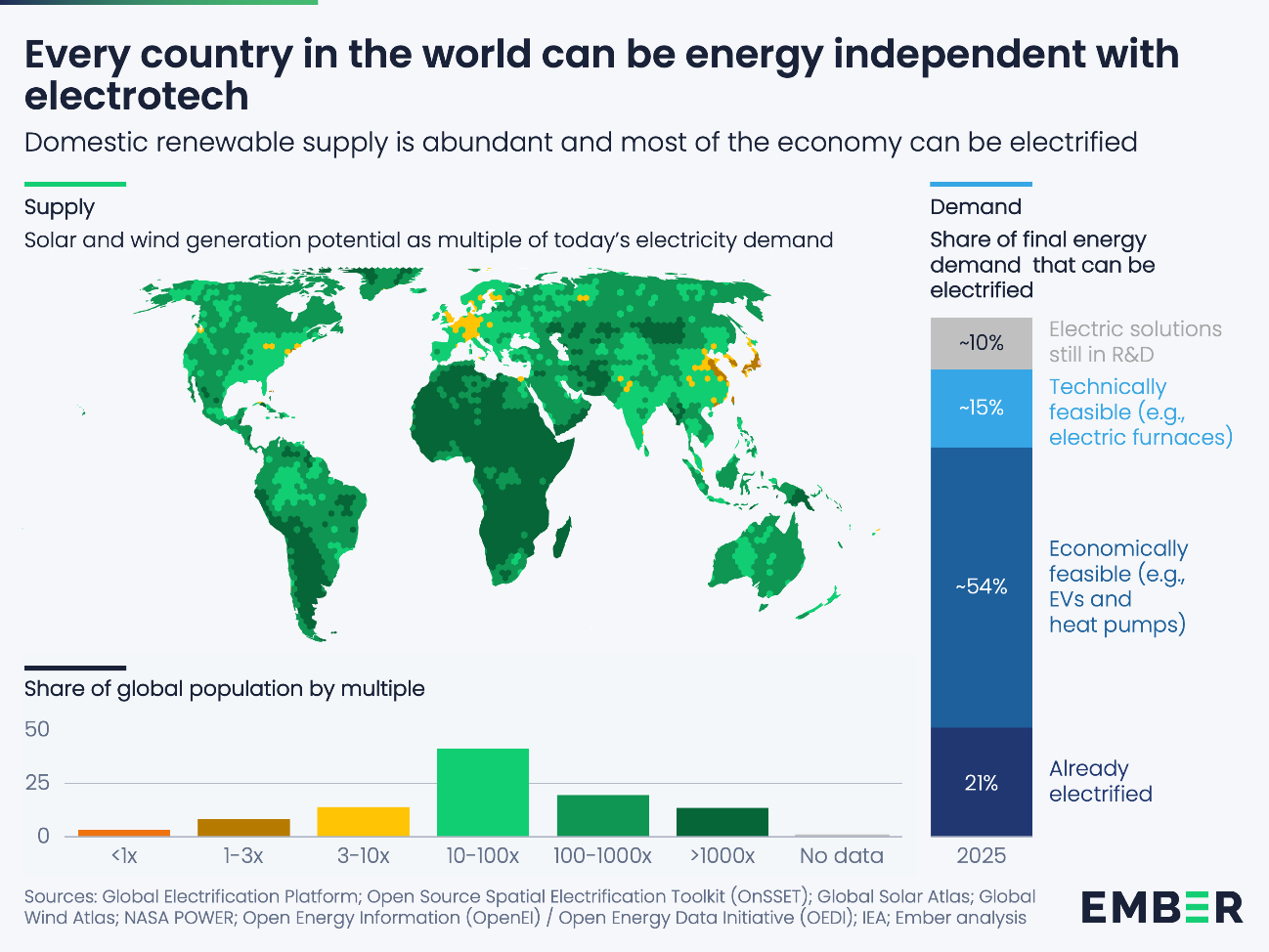

The technology to slash fossil fuel import dependency already exists. Proven technologies can electrify over three-quarters of the global economy. And every country in the world has enough wind and solar potential to power that demand with home-grown energy.

Three levers do the bulk of the work. Solar and wind replace imported fossil-fuelled power generation. Electric vehicles replace imported oil in road transport. Heat pumps replace imported gas and oil in heating. If all three were scaled to replace imported fossil fuels in their respective sectors, importers could reduce their bill by around 70%.

The superlever today is EVs. They are price-competitive with combustion cars and readily available. Replacing imported oil used in road transport with EVs would reduce importers’ bills by over a third – around $600 billion per year. The second-largest lever is renewables, able to reduce importers’ bills by a fifth.

Sceptics argue electrotech merely exchanges one dependency for another – Saudi oil out, Chinese solar panels in. But this is to confuse renting and owning. A solar panel, once installed, produces power for three decades with no fuel cost, no price increase or supply risk. An EV, once bought, runs on domestic electricity, which can largely come from local wind and solar. Fossil fuels require continuous imports. Every barrel, every cargo, every pipeline flow must be repeated, indefinitely.

Electrotech is already at the scale and price to cushion fossil shocks

In the world of electrotech, four years is a long time. Since the 2022 energy crisis, electrotech has become cheaper, better, and more readily available. It is already at a scale to cushion part of the Hormuz shock.

Solar panels have halved in price since 2022. Annual solar installations have nearly tripled in four years. Battery prices have fallen by 36%. Annual deployment of grid batteries is seven times higher. The total cost of dispatchable solar – panel plus battery – is now just $76/MWh for countries that import tariff-free. EVs are increasingly at sticker price parity with combustion cars, and EV sales have doubled since 2022.

Electrotech is now operating at a scale that can ameliorate a major crisis like Hormuz:

- The growth in global solar generation in 2025 alone could displace gas-fired electricity equal to all LNG exported through the Strait of Hormuz that year. In 2025, 82 million tonnes of LNG went through the strait; used in gas power plants, that could generate about 600 TWh of electricity. The IEA calculated that global solar generation rose by more than 600 TWh in 2025.

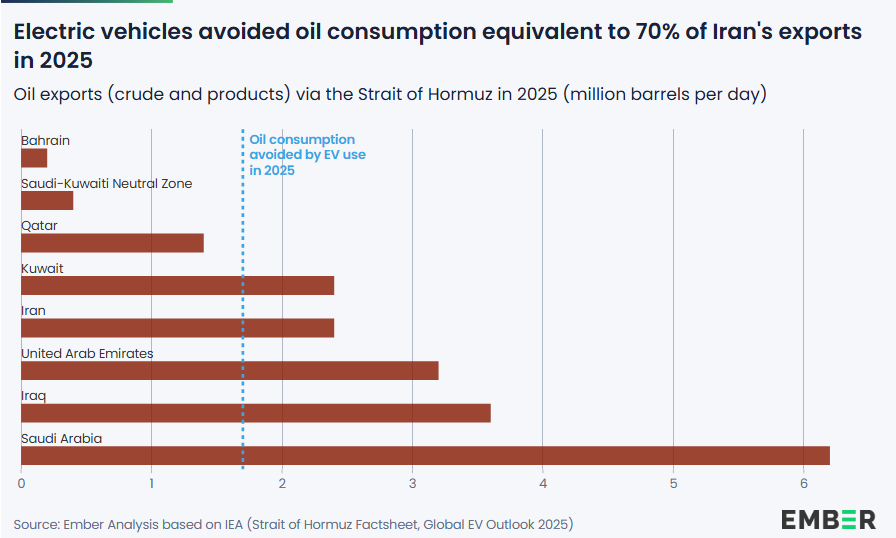

- Based on global EV sales, we calculate that electric vehicles displaced 1.7 million barrels per day of oil worldwide in 2025 – up from 1.3 million barrels in 2024 – not yet approaching the 20 million barrels per day of all oil demand that passes through the Strait of Hormuz, but still nearly as much as Iran’s 2.4 million barrels per day of exports.

Across many countries, rapid EV deployment is already slowing the growth of oil demand. Without this wave of electrification, petrol demand today would be significantly higher — particularly in fast-growing Asian economies where mobility demand continues to expand.

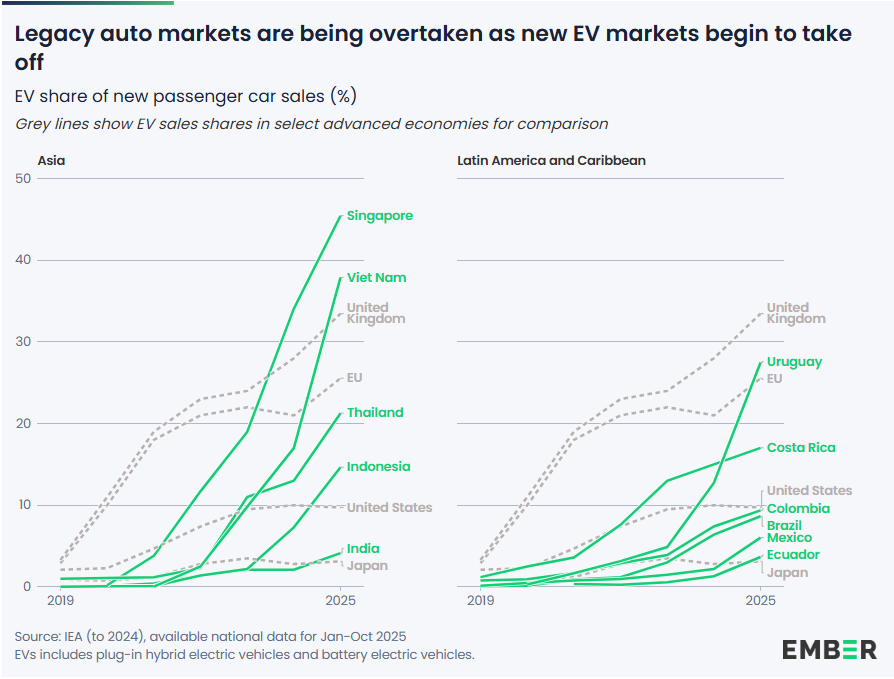

Ember analysis shows that 39 countries now have an EV sales share of more than 10%, up from four in 2019. Across regions, multiple emerging markets are surpassing advanced economies in their EV sales share. Viet Nam (38%) and Uruguay (27%) had a higher share of EV sales than the EU average in 2025 (26%). Thailand (21%), India (4%), Mexico (6%) and Brazil (9%) now have a higher EV sales share than Japan (3%). And Indonesia’s EV sales share reached 15% in 2025, overtaking the US (10%) for the first time. China reached over 50% EV sales share for the first time in 2025.

The current crisis adds further momentum. Higher and more volatile fuel prices strengthen the economic case for EV adoption, motivating faster uptake and reinforcing their role in curbing future oil demand growth.

The savings from electric vehicles are already being banked. With oil at $80 per barrel, China saves over $28 billion a year in avoided oil imports through its current fleet of EVs alone; Europe about $8 billion per year and India $0.6 billion per year.

Wind and solar go further still. Across net coal-and-gas importers in 2024, the import bill reductions run into the tens of billions: roughly $60 billion for China, around $9 billion each for Germany and Brazil, and $5-7 billion in Spain, the UK and Japan.

3. The lasting consequences

Beyond the immediate shock, this crisis will reshape energy markets in three ways.

This is Asia’s Ukraine moment

Russia’s invasion of Ukraine that began in 2022 galvanised Europe into action to reduce its dependency on Russian fossil fuels. Four years later, the US-Israel war with Iran will inspire Asia to reduce its dependency on imported oil and gas. The numbers are similar: in 2021 Europe imported around a third of its gas demand from Russia; in 2025 Asia imported 40% of its oil demand through the Strait of Hormuz.

But Asia enters this moment with an advantage that Europe did not have. Solar, wind, batteries and EVs are much cheaper and more readily available than they were in 2022, making the switch far more affordable. And where fossil fuel imports leak money out of the economy indefinitely, building up domestic electrotech manufacturing keeps that spending at home. Countries like India and Viet Nam are already showing the way. For Asia, this is not just a crisis to weather but an opportunity to convert fossil dependency into economic strength.

The prospects for LNG demand growth in Asia are over

As we noted last year in our Electrotech Revolution report, there is a battle between gas and solar for the future of electricity generation in Asia. At a stroke, this war has dramatically weakened the case for LNG.

The bull case for LNG was that it would be Asia’s transition fuel: cleaner than coal, available at scale, and secure. That thesis is now much weaker. Countries will be carefully considering the security of building long-term import infrastructure around a commodity that can see dramatic price spikes and supply risks.

Meanwhile, the alternative is already cheaper. Thanks to the collapse in solar and battery prices, Asia can now buy dispatchable solar at less than $80/MWh, with no fuel cost and no price risk, versus LNG at prices set by the next geopolitical crisis. Existing long-term LNG contracts become a liability, not an asset.

Peak oil demand is coming forward

For years, the International Energy Agency has been bringing forward its view of when oil demand will peak. A decade ago, it saw no peak before 2050 at all. Then it forecasted the late 2030s, and then 2030. Its latest forecast put it at 2029, at around 106 million barrels per day (mbpd), not much above 2025 levels of 104 mbpd. Even China, the largest growth market for oil over the past decade, saw demand fall in 2025 as electric vehicles displaced consumption.

This crisis is accelerating that trajectory. It is both curbing oil demand directly and sharpening the incentive to move away from oil altogether. The IEA has already cut its 2026 oil demand growth forecast to just 0.6 mbpd, and that is unlikely to be the last revision. As so often, a crisis can bring a peak sharply forward. We may well be at that peak now, in 2026. For a while, demand may simply bounce along that level. But if the closure of the Strait of Hormuz is prolonged, the plateau may turn quickly into structural decline.

Conclusion

At some point the Strait of Hormuz will reopen. Prices will ease. The crisis will fade from the headlines. But the structural logic will not change, and the next disruption will not be long in coming. Every year of continued fossil fuel import dependency is another year of exposure to a system that has shown, repeatedly, that it cannot be relied upon. The technology to end that dependency exists. The only question is how many more crises it takes. The countries with the foresight to invest in electrotech now will be better able to weather the next storm.

***********

Supporting materials

Methodology

Sources

This analysis relies primarily on the following data sources. Unless otherwise stated, figures correspond to the most recent data available. Global energy data are drawn from the IEA World Energy Balances, the EIA, and Ember. For LNG-specific data, this report relies on the Energy Institute’s Statistical Review of World Energy and GIIGNL’s annual reports. Global fossil fuel trade is analysed in value terms using the UN Comtrade database. Additional economic and population data are drawn from the World Bank.

Calculation on EV avoided oil consumption

The International Energy Agency showed the global electric vehicle fleet avoided the consumption of 1.3 million barrels per day of oil globally in 2024, and with the growth in EV sales in the last year, Ember calculates this has now risen to 1.7 mbpd. In comparison, Iran exported 2.4 million barrels of oil and oil products through the Strait of Hormuz last year.

Acknowledgements

Authors: Kingsmill Bond, Sam Butler-Sloss, Antoine Issac, Dave Jones, Kostantsa Rangelova, Daan Walter.

Contributors: Hannah Broadbent, Rocío Rodríguez Almaraz, Chelsea Bruce-Lockhart.Cover image credit: Ralf Hahn / Getty Images.

***********

Introduction/source of this column: Ember Energy Research (EMBER):

Ember Energy Research (EMBER), a UK-based energy think tank, takes an evidence-based, solutions-oriented approach to building an energy system that benefits everyone (driving the transition to clean energy).

Acknowledgments: We extend our sincere thanks to the author, Daan Walter, Principal at EMBER, UK, for granting permission to reproduce this valuable article.